Background

A fintech startup had an innovative approach to savings based on rock-solid principles: automation and paying yourself first. They were making a huge difference in customers lives by bringing complex automation strategies to populations which struggled to set these up manually, including high-turnover part-time employees at big box retailers and restaurants.

Challenge

Out the gate, this partner brought one of the hardest challenges in behavior change. How do you get people to save for tomorrow rather than spend today? Beyond that, we faced another issue: regulators and financial partners place significant restrictions on the product and design that don’t exist in other industries. With limited room for experimentation, there was a mandate to increase the percentage of people who successfully create automated savings programs and raise their probability of a secure financial future. The product was incredibly effective if people actually got it set up, but restrictions from financial partners and regulators chipped away at the user experience over time and made it cumbersome. The team needed a fresh approach with a limited toolkit. A white-labeled and heavily regulated product meant that many conventional methods to improve engagement were restricted.

Approach

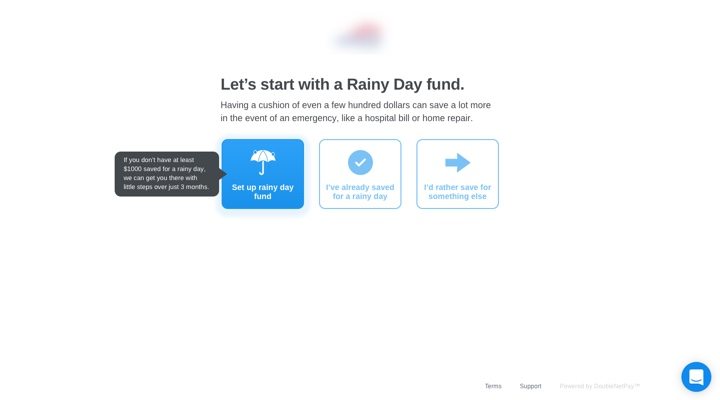

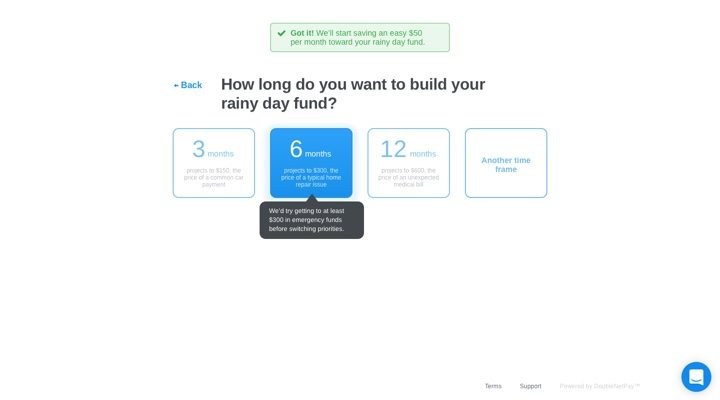

There were two key approaches to this problem. The first was reducing the complexity and cognitive load of creating an automated savings plan by subtly removing choices, adding smart defaults, and using simple language. The second was subtly altering the participants’ pre-existing beliefs about implicit and descriptive norms around saving.

Some of our contributions included:

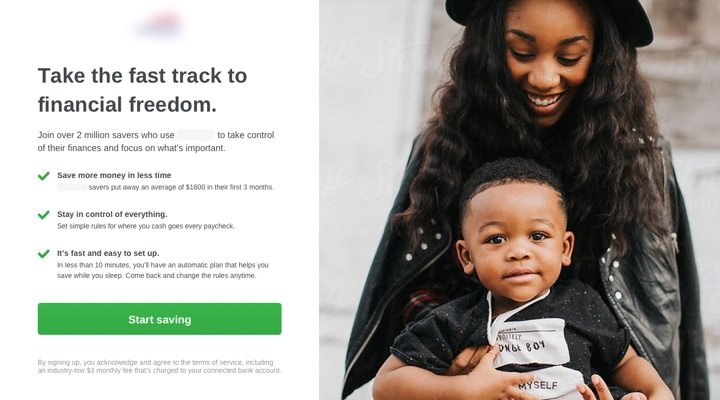

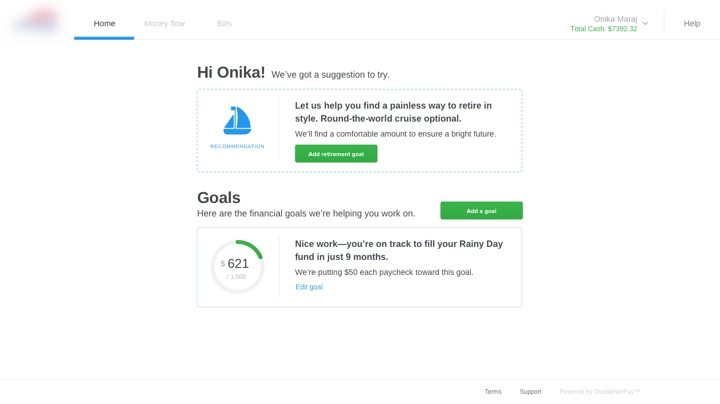

Simplified savings plan creation which allowed a fully automated retirement plan to be set up without a user typing numbers, manually choosing savings rates, or doing any math whatsoever

Revamped copy leveraging best practices in behavioral economics, like loss aversion and social proof

Reimagined design language for better responsiveness

Web application prototyping

Retention and reactivation messaging strategy for email & SMS

IMPACT

Results

The startup saw dramatic improvements in the savings account setup experience and underlying metrics, and ultimately chose to apply similar principles to its entire product suite from debt reduction to automated bill pay to retirement planning.